So you want to save on taxes in Pakistan?

How investment in mutual funds can save you a lot on taxes

Continuing the mission for simplifying and demystifying investments for everyone, the current issue focuses on tax savings. If you haven’t subscribed to the newsletter, you can subscribe here and just make more money by following very simple rules, and common sense.

No one likes to pay taxes, especially when you’re salaried, or running a small business, and the government instead of expanding the tax net just keep on taxing the small chap more. However, you can save up on some of the taxes you pay, and reduce your overall tax burden through investments in mutual, or pension funds. This is not a scam. This is a genuine legal incentive designed to encourage savings in mutual funds. Taxes and death are the only two things certain in this world. Taxes are only expected to increase going forward.

What is a mutual fund?

Let’s say you save a small amount every month. Instead of identifying individual stocks, or securities to invest in, you can directly invest in a ‘mutual fund’ every month, which on your behalf invests in a large number of stocks or securities. For the sake of simplicity, there are two types of mutual funds, equity funds, and income funds.

The equity funds invest in the stock market and hence are considered to be risky. The fixed-income funds invest in a mix of government securities, or debt issued by various companies, and provide a stable return, with the minimal potential of loss. In the case of mutual funds solely investing in government securities, the risk is very low. More details have been provided in this piece here.

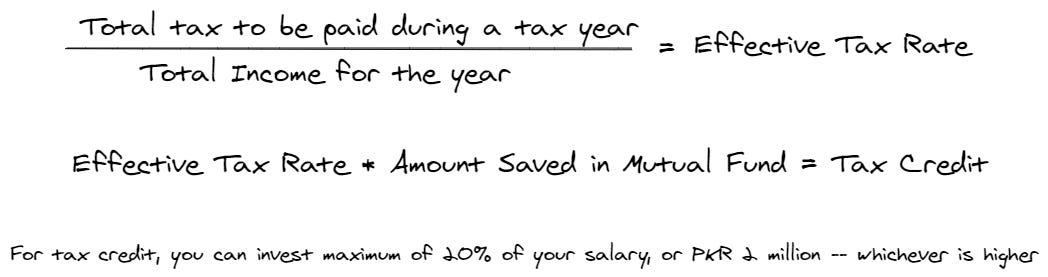

So how do I save tax?

By simply investing in mutual funds. That’s it. The tax code allows individuals to get a ‘tax credit’ in proportion to some amount that they have invested in mutual funds. Let’s look at an example here. Let’s say you have a monthly income of Rs. 200,000, which means you’re paying taxes of Rs. 15,000 on a monthly basis, and about Rs. 180,000 on an annual basis. You can add any bonuses you get to this as well. A nifty tax calculator is available here – no idea about its authenticity. But you should have an idea regarding how much tax is deducted as shown on your monthly salary slip.

Your effective tax rate in this case is, 180,0000/(200,000*12) = 7.5%. An amount up to 20% of your annual salary is eligible for tax credits – which in this case is PKR 480,000. In-effect, you can get tax credit of up to 7.5% * 480,000 = PKR 36,000. That is almost 73 days of taxes that you saved, and which you can well use to invest more, or just throw a small party, or whatever.

But how do I do it safely?

If you don’t know where to invest, just invest in a money market mutual fund. The profit that you get would be higher than what you get from a bank, and you get a tax credit as well. However, depending on your age, and your stage of life, you can always move towards riskier investments – but for starters, just getting a sweet tax credit through a money market fund is totally fine.

Let’s say you invest 480,000 right now, in a money market mutual fund. The profit rate is roughly ranging around 6.5%. Your profit for the next two years would be roughly PKR 64,400. Add in a tax credit of roughly PKR 36,000 as calculated above — and you have a net profit of PKR 100,000+.

When can I get my money back?

A key condition for this incentive is that you should invest for at least two years. These are your savings, you are getting a profit and tax credit on them, so nothing to worry about. But if you redeem within two years, you may have to return back the tax credit. A trick here is to keep revolving this amount for every two years. Let’s say you invest PKR 480,000 right now, and get a tax credit this year. Two years later, you can redeem the amount, and reinvest to get a fresh tax credit. In this way, you can develop a perpetual tax credit cycle till the time the incentive is removed by the government.

How do I get my money back?

The Government staying true to its extortionate roots does not really give anything back to you in cash. Why were you expecting this anyway? If you’re salaried, you go to the finance or accounts department of your organization which processes your salary, and request them to adjust your tax accordingly. Similarly, if you’re self-employed and file your taxes independently, you can adjust your tax credit from the total tax that you have to pay.

So when do I get started?

Like right now. Today. The tax credits are managed for each individual tax year, which ends on 30th June. So you would still have two more salaries that you can get in May and June of the current tax year. Using the example above, you would be paying PKR 30,000 in taxes over May and June. Meanwhile, if you invest PKR 400,000 in a mutual fund right now, you can save the PKR 30,000 in taxes.

How do I get started?

Find a money market mutual fund, and invest in it. A detailed list of mutual funds is available here. Feel free to drop a comment, or message if any more details or information is required. Money market funds are currently giving a profit in the range of 6 to 7% nowadays on an annual basis – it’s not a lot, but it’s higher than what you get in a savings account in your bank, and it allows you to get a sweet tax credit.

If you have savings lying in a bank, just move them right now and get an easy tax credit. Can’t get simpler than this.

P.S. There can be more tax savings through a pension fund, but we will cover that some other time.

I invested 100k in islamic income funds in may, can i apply for tax credit in this tax year? And what is the procedure?

Excellent article Ammar. Very easy to understand.

One thing I wanted to point out is that when talking about savings accounts, wouldn't it be better to inform the reader that the value of savings will go down due to inflation. However, value of investments in mutual funds will also keep on fluctuating. Folks might get an idea that the principal value stays intact in case of mutual funds.