But where do I invest?

Developing a framework for asset allocation or portfolio development

In the third iteration of Munaafa, let’s drill down into what an ideal portfolio should be like, depending on your age, your intended time horizon, etc. If you are new here, please review the previous newsletters to understand how to go about investing, and developing a portfolio.

As a thumb rule, a long-term horizon allows one to take more risk, and that ability to take risk declines as the time horizon shortens. Wherever applicable, I will also cover various Shariah Compliant options available. It is possible to create a high-return diversified portfolio while staying within the tenets of Shariah.

Let’s say, you need to save for the university education of your children, you’ve got a long-term horizon, which allows you to take more risk. Meanwhile, if you want to save for a vacation in the next six months – that is a fairly short-term horizon, and you can’t take much risk with it. But why is there a link of time horizon with risk? It’s simple. A longer-term horizon allows one to recover from any losses over the years, and so on. Meanwhile, in case of loss during a short-term horizon, you can’t really recover from it, unless you hold your losses, and hope it recovers in the future.

Create Risk Buckets

Zoom out. Think about it. What are your short-term financial goals, and what are your long-term goals. You need to create risk buckets in your head, or on a piece of paper. Short-term goals go in the low-risk bucket, long-term goals go in the high-risk bucket. Another long-term goal that we often don’t think about is planning for retirement, which in the local context is mostly expecting a government pension, or relying on your children. The government doesn’t have funds to dole out pensions anymore, and why would you be a burden on your children anyway? Invest for your retirement. You need to compartmentalize your goals and your risks. Let’s just park this on the side now.

Let’s say we now have two buckets in our heads. We need to ‘invest’ those in various assets (or investments). They need to be invested in a manner such that you don’t take any excess risk, and your return can be maximized. Easier said than done, but more often than not, people get stuck in bad investments, because someone sold them a bad plan, or they got stuck with some family, or friend they trusted in a bad deal. Let’s look at an insurance policy, the darling of every household. It is a highly inefficient product, where you as an investor don’t break-even till the seventh year (in most cases). You may think you got a good deal, but you did not. More on insurance policy math in a subsequent piece.

Avoid Concentrated Land Investments

Similarly, buying a piece of land in an undeveloped suburb somewhere such that it develops and pays off your child’s university fee is a super high-risk investment. Sometimes the land develops, sometimes it doesn’t, and sometimes there is some incident of landgrab, and so on.

Locking yourself in an illiquid (something that you cannot sell without taking a significant loss) asset, while allocating a significant portion of your wealth to it, in hopes that it may cover some financial goal in the future, is bad financial planning. This is high-risk, and you’re at mercy of most likely a scrupulous land developer in a largely unregulated market. There is an adage in the local context that the price of land only goes up – empirically that is not true. Detailed math on this at a later stage.

So where do we invest? What are the options available? I’m detailing various options available, which can be combined to create a portfolio that aligns with your goals, and risk buckets.

Bank Deposits

These provide the lowest return, and in many cases don’t even provide a return. You most likely get your salary in a bank account, and at times you just let the funds stay there because you don’t know what to do with them. The Bank makes hay on your funds. If you have placed funds in a ‘current account’, the ‘cost of funds for the Bank is ‘zero’, while it lends that out at say 8 to 9 percent. Why should you let the Bank earn more with your hard-earned income when you can do the same. As a thumb rule, funds in Banks should just be enough to cover any emergency cash requirements. Any surplus should be invested.

It is understood that if you’re early in your career, or even mid-way through, there isn’t much cash left. Putting aside some x percent every month does wonders for savings. Even putting aside PKR 1,000 every month is a start. Even if Bank offers you a high return on a ‘term deposit’, it’s better to compare that rate with Government Bonds, or Treasury Bills, a high likelihood you can get a better return elsewhere.

Treasury Bills

This is how the government borrows money for the short-term, say for 3-months, 6-months, or 1-year. At maturity, the government gives you back the money – but you can always invest again. In practice, you deposit funds in a Bank, and the Bank uses those to lend to the government. Using the example above, your funds in the current account (at zero cost) can be deployed by the Bank in treasury bills at 7.5%+. Why shouldn’t you do the same, and cut out the middle-man, that is the Bank? You can either invest directly in treasury bills or through a ‘money market fund’. We will cover the operational modalities in the next iteration.

There is no shariah-compliant option for the same, however, a close alternative is to go for shariah-compliant money market funds.

Government Bonds

This is how the government borrows money for the long-term, say for 3-year, 5-years, or 10-years. You lend the government some money, they give you an interest payment every six months. It’s as easy as that. At maturity (at the end of 3, 5, or 10 years, you get all your money back. You can either directly invest in government bonds, or you can go through a dedicated income fund. More on the modalities in the next iteration.

Shariah-compliant option for this is Ijara Sukuks, which is basically government debt but backed by some tangible asset, such as a motorway, airports, parks, etc.

National Saving Schemes

Pretty much everyone would be aware of how government borrows through Defense Certificates, Saving Certificates, etc. Each certificate has a defined maturity, which can be 1-year, 3-years, 5-years, or 10-years, and a corresponding interest rate. As a thumb rule, the greater the maturity, the higher the interest rate. Once again, completely backed by the government so totally safe.

There is no shariah-compliant option for the same.

Corporate Bonds

This is how companies borrow funds, whether public or private companies. The return on these is higher than the government, and so is the risk. It may be possible that a company borrowing funds go into default and is not able to pay back your funds, hence the higher risk. The higher risk is compensated by a higher return. How to navigate through corporate bonds, would be covered in a subsequent piece.

Equities

We are now in the high risk-high return territory. Equities are popularly called ‘stocks’ or ‘shares’. By buying a share, you become a partial owner of that company, and when a company grows, or generates a profit, being a shareholder, you have a share in that as well through the Pakistan Stock Exchange (PSX).

But not all companies do well – some do extremely well and generate a lot of profits for their shareholders, while some are not able to do well whether due to external factors, or bad management, and you can lose all your money with them.

Within equities, you need to further diversify – either buy shares in multiple companies, or just invest in a mutual fund, or an exchange-traded fund. More details on this later – but broadly speaking, as the overall economy grows, companies, and their profitability grow as well.

Precious Metals

In the local context, there is this overwhelming pressure to save in gold, or even worse through buying jewelry. Another misconception here is that price of gold only increases, which is not true at all. Gold is an alternate asset class, and should not make up 5 to 10 percent of your portfolio. Even if it is a part of your portfolio, make sure it is in physical gold bars, or biscuits, and not jewelry. If you buy jewelry from your trusted jeweler, and sell it back in ten days, chances are he is going to deduct 15-20 percent of the value as ‘making charges’. You’re in a straight loss here. Better to buy physical gold, no matter how small denomination (3 grams, or more) – you’re better off than buying jewelry.

Real Estate / REIT

Everyone is selling a plot file these days. How many of these may actually be developed, that’s a separate story. You may be left holding a file with worthless paper while the developer lives the rest of his life in the Bahamas, or worse, Nova Scotia. Figure out why you need real estate, if it is for saving, then you compare its returns with the options above. If it is to live, then work out how you can leverage your position, and whether it is cheaper to rent or buy – high chance it is cheaper to rent, than to buy. More on this later.

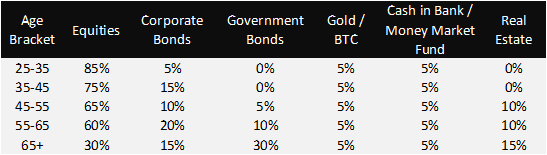

So how should I allocate?

Assuming that you have a long-term view of things, this table below provides a rough idea regarding how you should be allocating your funds, or develop your portfolio. Each individual may have a different iteration — but broadly the direction would remain the same. I have also added some Bitcoin (BTC) in it for some flavor — high risk, highly speculative, and high return — more on this letter.

I hope this issue wasn’t too complicated. In the next issue, I will try to cover how exactly to start investing — since we now have the relevant framework in place.

If you like this post, share away.

This is a great series of writings. Really appreciate this effort. Where would you put insurance plans in this list?

Very Informative post. The dilemma is that not many are aware of Investing Dynamics. Can we have a collaborative post on the same on https://www.businesstribune.com.pk/ ?